While most business owners may be familiar with the 401(k) plan, much fewer have heard of the cash balance plan. This is despite the growing popularity of these plans since the Pension Protection Act of 2006. To be perfectly honest, however, cash balance plans are somewhat difficult to wrap your brain around given their “hybrid” nature; that is, cash balance plans look like defined contribution plans (like a 401(k)) but are actually a defined benefit plan (like a pension).

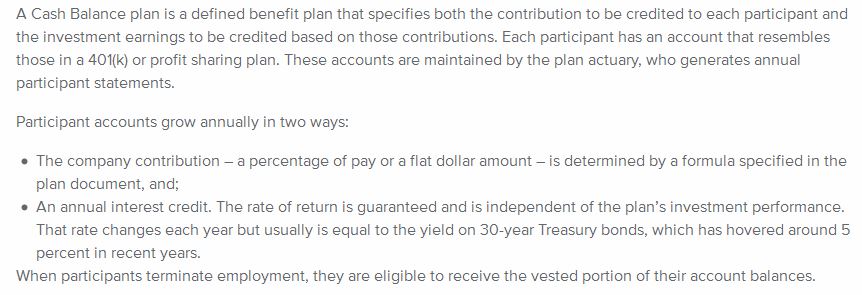

Kravitz, a cash balance plan design firm, has a straightforward description:

(Source: Kravitz)

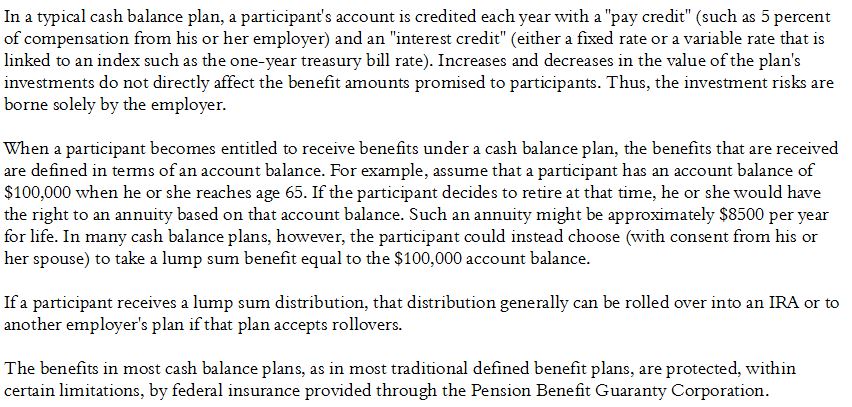

So how do these plans work from the participant perspective? As it turns out, the Department of Labor has a pretty good consumer bulletin on cash balance plans:

(Source: Department of Labor)

The value to the business owner — aside from the tax benefits — is the ability to contribute a much larger amount to the cash balance plan as compared to a 401(k). For example, a person born in 1970 could contribute up to $111,322 (based on 2016 limits). In addition, this person could contribute an additional $18,000 to the 401(k) plan for a total retirement savings of $129,322. This is quite an improvement over the maximum all-in contribution (from employee and employer) of $53,000 for a standalone 401(k).

A consistent record of positive cash flow and profits is a prerequisite, however, since the company is obligated to fund the annual contributions. Additionally, a quick-and-dirty rule of thumb is that if 70% of the company contributions going into the plan is for key stakeholders (e.g., owners), the tax savings for those key personnel makes the cost of funding and administering the cash balance plan worthwhile.

Cash balance plans should be used alongside 401(k) plans, not in place of them, and are more expensive to setup and manage. Business owners should talk to their financial advisors about the cost and benefit of these plans, especially within the context of succession or exit planning.

—

Mention of products, providers, or services does not constitute an endorsement or relationship.

The information presented here is for informational purposes only, and this document is not to be construed as an offer to sell, or the solicitation of an offer to buy, securities. Some investments are not suitable for all investors, and there can be no assurance that any investment strategy will be successful. The hyperlinks included in this message provide direct access to other Internet resources, including Web sites. While we believe this information to be from reliable sources, Targeted Wealth Solutions LLC is not responsible for the accuracy or content of information contained in these sites. Although we make every effort to ensure these links are accurate, up to date and relevant, we cannot take responsibility for pages maintained by external providers. The views expressed by these external providers on their own Web pages or on external sites they link to are not necessarily those of Targeted Wealth Solutions LLC.